Many of the companies with which we come into contact in the course of our business are (or, were) rapidly growing companies. They were started some years earlier, and have been growing pretty steadily since their founding.

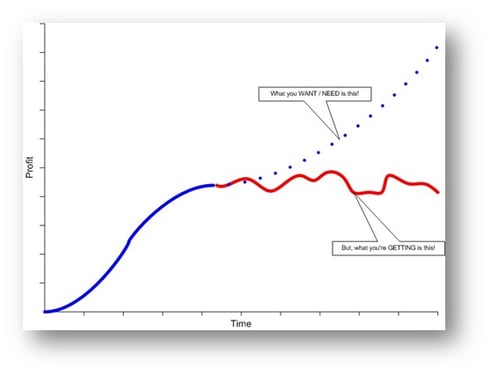

However, many times we are called in because the growth curve has become unsatisfactory. Perhaps the companies' profits have been relatively flat for several years. Or, in some cases, profits have turned negative. As a result, executives and managers are looking for new ways to return their companies to a growth trajectory.

All too often, they come to us with the sole thought in their minds that some new technology is what is needed to put them back on the path to the profitability that they desire. They have in their minds this concept that technologies are something that can be "poured" into their company like a miracle engine additive that will help their company "run smoother, last longer and get better mileage."

They frequently have such thoughts when the challenge they are really facing is a common struggle to so many companies: they are struggling to leap the chasm between "entrepreneurial" and "enterprise."

Why is there such a struggle? And why is it such a common struggle for companies when they reach a certain threshold in their growth?

Entrepreneurial Thinking

When entrepreneurs start their companies, their thinking about how to make more money is very un-complicated.

When entrepreneurs see an opportunity, they are generally able to quickly and incisively do an analysis that incorporates the following general line of thinking:

- Revenues (R) – "If we can take advantage of this opportunity, I believe we can gather in about $R in gross revenues in the first year from our customers."

- Truly Variable Costs (TVC) - "In order for us to take advantage of this opportunity, we will have to pay out about $C for each unit we deliver to our customers."

- Investment (I) – "Before we can start collecting our Revenues, we will need to invest about $I to get the ball rolling." (This investment might include capital equipment, inventories, or other.)

- Operating Expenses (OE) – "Once we get the ball rolling, we will have some ongoing expenses. We will need to pay out about $OE each month over the first year of our operations."

There are some important things we should note about this back-of-a-napkin kind of evaluation that is quickly performed by entrepreneurial minds.

First, note the repetitive use of the word "about." In these kinds of evaluations, being approximately right is key. There is no need whatsoever to hone these numbers to increasing levels of accuracy.

After making rough calculations, the net opportunity can be assessed as being a certain size and can be scaled by order of magnitude. If the net opportunity calculates to a few hundreds of dollars, the risk may not be worth it. However, if the net opportunity calculates to tens of thousands, or hundreds of thousands, of dollars, they may wish to pursue it immediately, lest it slip away.

Importantly, also note that there are no needless allocations of expenses to products or services delivered. The entrepreneurial mind tends to recognize intuitively that every dollar of R minus TVC above OE is profit. Allocations add nothing to their ability to evaluate the opportunities available to them. Read How to Save 392 Hours per Month.

Calculating the "Net Opportunity" Value

The net opportunity value emerges from a formula that may never be articulated by the entrepreneurs, but it exists in their minds nonetheless. That formula may be stated as the following for PROFIT:

P = (R – TVC) – OE

Where…

- P = Profit

- R = Revenue

- TVC = Truly Variable Costs

- OE = Operating Expenses

If some not insignificant investment is involved, then the calculation for return on investment (ROI)—still simple enough to be done in a coffee shop on a napkin—becomes:

ROI = ((R – TVC) – OE) / I

Where, I = Investment

(See more on Throughput accounting here.)

Continued Growth

Most entrepreneurial organizations continue to use these formulas (perhaps, and frequently, never articulated as such) to rapidly evaluate profit opportunities. The application of this approximately right methodology becomes a key factor in rapid, accurate decision-making that leads to generally high return on investment and not uncommon double-digit compound growth rates.

Such companies generally follow this pattern of decision-making until they reach a certain size and level of complexity. (Here we use "level of complexity" to describe the size of the enterprise as defined primarily by the number of active participants or the number of transactions in the daily of execution of the business—that is the number of employees and trading partners involved.) As transaction volumes increase, so does the need for accounting and other systems to track the various aspects of the transactions. Ultimately, an Enterprise Resource Planning (ERP) system is generally implemented. With the ERP system comes the accumulation of historical data and the ability to perform relatively complex analyses and reporting on the accumulated data.

Also, accompanying such growth and complexity of systems, come the people who believe it is their responsibility to use these accumulating mountains of data to "improve decision-making" through complex analytics. Applying GAAP-compliant methods (which were designed for external financial reporting, and not for management decision-making), they begin to make complex what used to be simple calculations on how and when to take advantage of clearly profitable growth opportunities.

Studying the Cadaver

The entrepreneurial mind is clearly forward-looking. Entrepreneurs tend to be able to be able to see opportunities on the horizon, envision a way to profit from those opportunities, and calculate—at least by order of magnitude—the dollar-value of the opportunities they see.

Now, encumbered by mountains of data and those they have hired to oversee and analyze these mountains of data, their focus is moved from forward-looking to a constant reconsideration of their historical data. (After all, that's was an accounting system is: it is a history-keeper designed for reporting the results of past operations. Such systems were never designed for management's day-to-day decision-making.)

These executives and managers—trying desperately to leap the chasm from entrepreneurial to enterprise—are now spending their time "studying the cadaver" of their organization in the vain hope of making decisions regarding future opportunities.

H. Thomas Johnson and Anders Bröms describe, far better than I could, the problems associated with focusing on "the cadaver" rather than the future in their great book, Profit Beyond Measure.

Studying the cadaver…is the prevailing management strategy. Influenced by the mechanistic worldview of the social sciences, late-twentieth-century managers view a business organization exactly this way. They operate businesses by imposing on them an artificial design that connects the organization's parts and then shows its interactions in linear quantitative terms, financial and otherwise. They view the financial performance of the business as the sum of the separate financial performance of each part. Anyone of these parts, they believe, can be added to or subtracted from the business with a predictable financial impact on the whole.

Quantity cannot explain, however, the internal operation of a natural system. It can only describe the natural system's external features.... Quantitative measurements give no insight…into why, or how, such natural systems function as they do. Measurements never provide understanding of the internal operation of a natural system. – Johnson, H. Thomas, and Anders Bröms. Profit Beyond Measure: Extraordinary Results through Attention to Work and People. New York: Free, 2000. Print. P. 48]

Restoring Focus

There is no mystery in what we do. We help companies trying to successfully leap the chasm from entrepreneurial to enterprise regain the vitality they formerly had by helping them regain their focus on the future. We help them see that management accounting and the analytics that benefit management decision-making are not the same as numbers and methods used for GAAP-compliant reporting on financial results.

We help executives and managers once again see that they methods they used as entrepreneurs to launch their business and gain so many early successes are still valid today. With business intelligence reporting tools these methods can be used to calculate the magnitude of any number of alternative improvement or growth opportunities, and even prioritize them for action.

We would like to store life to your organization and supply chain, too, by helping you see your future afresh and end your focus on the cadaver of your history.

Richard Cushing is a Supply Chain expert with a focus on Demand-driven supply chains. Read more of Richard Cushing's blogs.